Self Employment and the new tax laws

There are millions of entrepreneurs in the US today and business is booming. The Tax Cut and Jobs Act (TCJA) provides businesses with a variety of changes in tax reporting. One of those changes that affect self employed individuals is the 20% deduction for pass-through entities qualified business income (QBI). The qualified business income deduction (QBI) starts in tax year 2018 and ends after 2025.

What is a pass through entity?

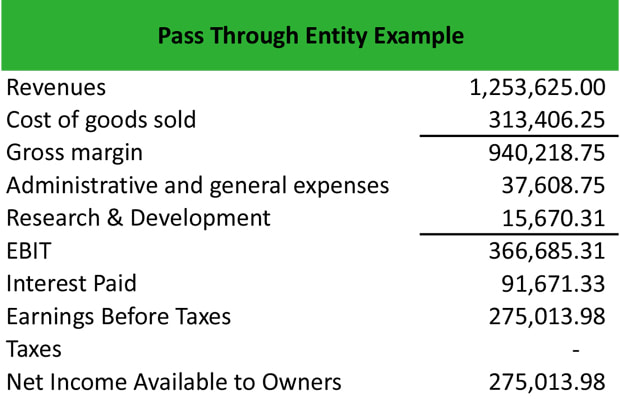

Sole proprietorships, partnerships, LLCs and S corporations are pass-through entities for federal income tax purposes. This means these entities are not subject to income tax. Rather, the owners are directly taxed individually on the income, taking into account their share of the profits and losses. In basic terms, that means a company passes its income on to its owners and doesn’t pay taxes on the income at the entity (or "company") level. Look at the sample chart below for an example of pass through entity.

How does it work?

Effective for tax years 2018 - 2025 a taxpayer is entitled to a deduction equal to 20% of the taxpayer’s QBI earned in a "qualified trade or business.”

The deduction is available to any taxpayer that is not a corporation. This includes:

The deduction is available to any taxpayer that is not a corporation. This includes:

- Individual owners of sole proprietorships, rental properties, S corporations, or partnerships, and

- An S corporation, partnership, or trust that owns an interest in a pass-through entity.